The Map is Wrong: Why the Next Great Art Collection Will be Built Outside The Western Canon

The Western art market has a concentration problem — and sophisticated collectors who notice it early will define the next generation of great collections.

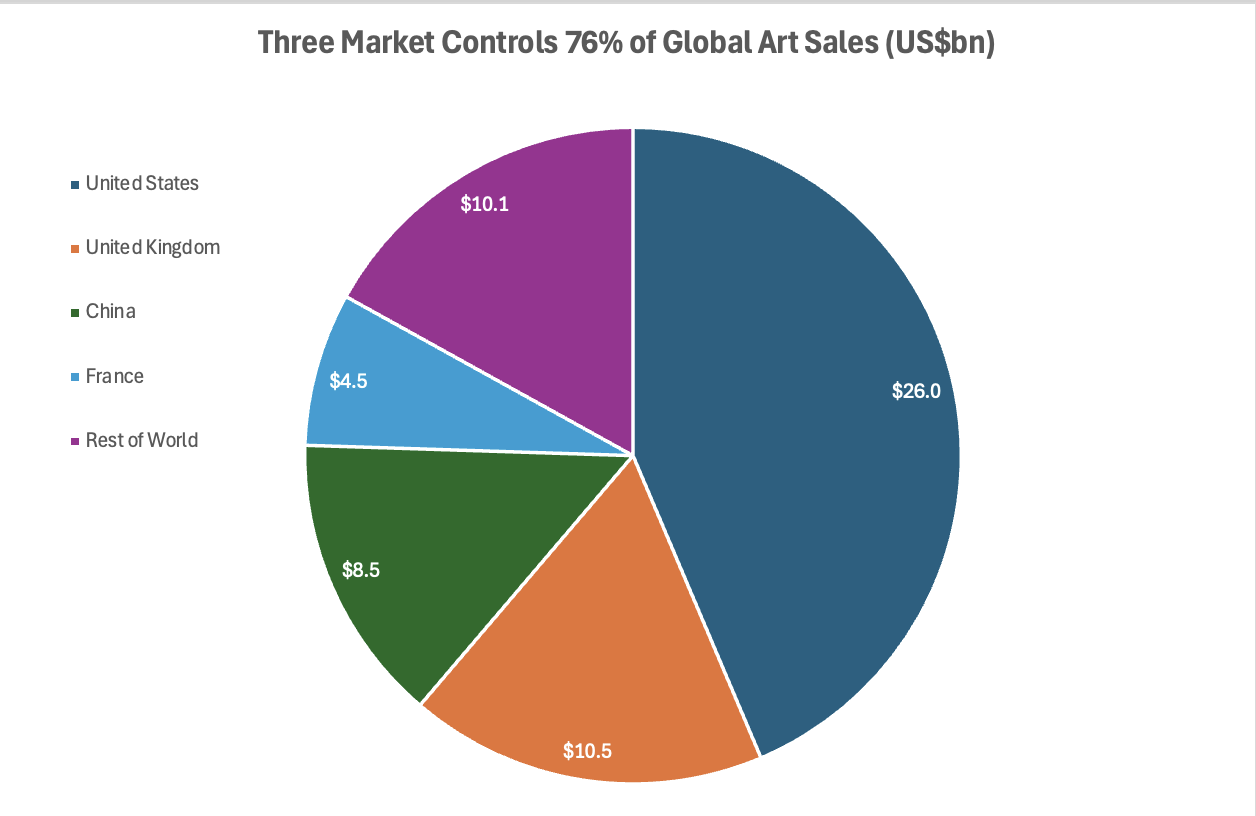

The global art market recovered in 2025, growing 4% to $59.6 billion. The US, UK and China together accounted for 76% of that figure. New York alone executed 78% of all works sold above $10 million. On the surface, this looks like confirmation that the incumbent geography is holding. The more useful read is the opposite: a market this concentrated, this late in its cycle, offers late entrants premium prices and first movers a narrowing window.

WHY THIS MATTERS

Asymmetric entry: Works by artists from the Gulf, South Asia and Sub-Saharan Africa trade at significant discounts relative to Western equivalents of comparable exhibition history — a mispricing that institutional endorsement will close.

Infrastructure before demand: Several sovereign-wealth-backed cultural economies are building museum infrastructure before a private collector class exists, creating a rare opportunity to acquire ahead of institutional validation.

Policy tailwinds: From India's recent goods and services tax cut on art to Saudi Vision 2030's cultural agenda, fiscal and strategic policy is now actively stimulating emerging art markets in ways Western markets have not seen for decades.

The Core Shift

The global art market is not stagnating; it is bifurcating. At the top, value is concentrating further: works above $10 million rose 30% by value in 2025, and the 50 highest-priced lots globally were almost entirely sold in New York. At the bottom, a different story is unfolding. Online art sales, now at $9.2 billion, are dominated by works priced below $50,000, with 63% of online auction value sitting in that range. Those buyers are not primarily in Manhattan. They are in Seoul, Mumbai, Dubai and Jakarta.

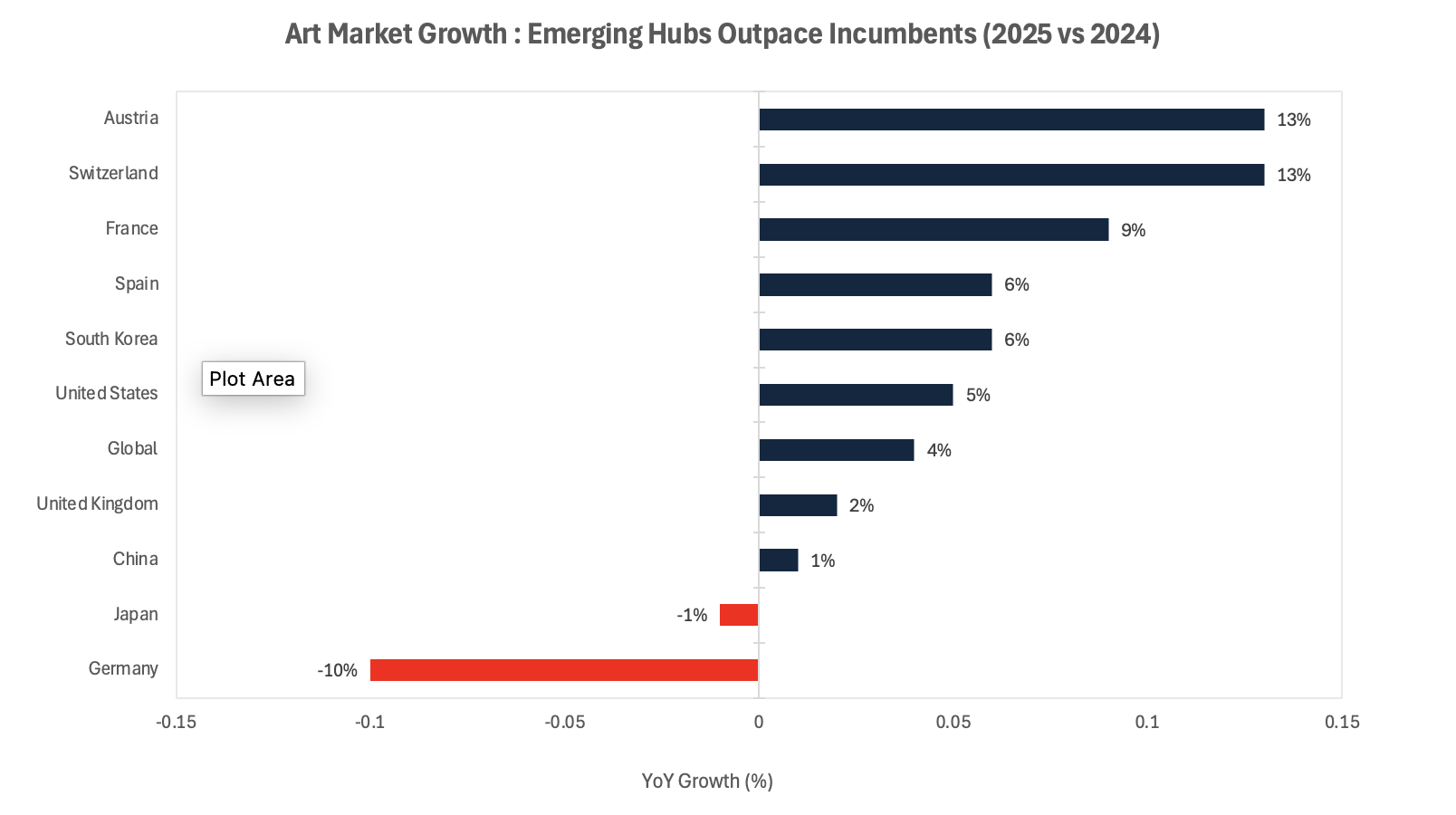

The data on geographic growth rates makes the structural shift plain. South Korea grew 6% in 2025. France grew 9%. Switzerland and Austria each grew 13%. Germany contracted 10%. Japan fell 1%. Hong Kong, historically Asia's pre-eminent art hub, saw contraction as Mainland China's share of the market slipped. The momentum is not with the incumbents.

Global art market sales by region, 2025 (USD billions). The US ($26b), UK ($10.5b) and China ($8.5b) together control 76% of the $59.6b global market — a concentration that has barely shifted in a decade. Source: Art Basel & UBS Global Art Market Report 2026.

The "Rest of World" at $10.1 billion is not a residual. It is the fastest-growing segment with the lowest valuation base. That is where collectors should be paying attention.

The Non-Obvious Mechanism

Every major Western art market followed the same formation sequence: private collectors accumulated first, dealers followed, auction houses liquified the secondary market, and museums eventually conferred institutional validation. London, New York and Zurich each took generations to build. The result is a deeply embedded premium for artists who passed through that system.

The Gulf states are running the sequence in reverse. The Louvre Abu Dhabi opened in 2017. The Guggenheim Abu Dhabi is under active development. Saudi Arabia's cultural strategy under Vision 2030 is explicit: soft power through cultural infrastructure, with state capital deployed ahead of any organic collector base. Qatar's collecting programme, executed primarily through state institutions, has already placed Gulf and Arab artists inside major global survey exhibitions.

This matters enormously for private collectors. When a state deploys institutional validation before private demand exists, it creates a brief window during which works by artists from that cultural geography trade at pre-institutional prices. The equivalent moment in the Western canon, when a Basquiat or a Koons could be acquired before the museum retrospectives recalibrated the market, has already closed. In MENA and South Asia, it has not.

India sharpened this case in April 2026. A painting by Raja Ravi Varma sold at auction for $17.9 million, setting a new Indian art record. India had also cut goods and services tax on art, an unambiguous policy signal that the government intends to stimulate domestic market depth. The collector class forming around India's technology and industrial wealth is not interested in collecting in the Western tradition; it is collecting Indian modernity with the confidence of a culture that does not need external validation to assign value.

Collector Implications

The portfolio logic for building in emerging markets rests on three distinct arguments, which are independent of each other and cumulative in effect.

Valuation gap: Works by artists from the Gulf, South Asia and Sub-Saharan Africa trade at meaningful discounts relative to Western contemporaries with comparable exhibition histories and critical attention. That discount is not permanent; it reflects geography of origin more than quality of work.

Currency and cost-of-entry dynamics: Acquiring from galleries in Mumbai, Nairobi or Riyadh involves operating in markets where the cost of relationship formation, fair participation and advisory infrastructure has not yet been inflated by Western art-market economics. The all-in cost of building a position is structurally lower.

Liquidity risk is real: Emerging art markets do not have deep secondary markets. A collector who needs to exit a position in Lagos or Jakarta within 18 months faces genuine execution risk. This is not an argument against building in these markets; it is an argument for building with a genuinely long horizon and treating the collection as a capital-illiquid cultural asset, not a near-term store of value.

Year-on-year art market growth by country, 2025 vs 2024. The fastest-growing markets are not the established incumbents. Source: Art Basel & UBS Global Art Market Report 2026.

Catalysts and Policy Outlook

The next 12 months present an asymmetric risk profile: the cost of moving early is time and relationship capital; the cost of moving late is the institutional premium that closes the window permanently.

0–3 month window: The Guggenheim Abu Dhabi is in active development, and any announcement of an opening date or inaugural exhibition programme would immediately recalibrate how Western auction houses price Gulf-associated works. India's April 2026 auction record for Ravi Varma is already drawing international attention to the Indian secondary market. Watch for whether Christie's or Sotheby's moves to strengthen India desk presence in response.

3–12 month window: Trump's tariff regime has inadvertently made the traditional New York-London-Hong Kong trade axis more expensive and administratively complex. Dealers are already pivoting toward localised collecting patterns: among the smallest dealers in 2025, 71% of sales went to domestic buyers, up 9% year-on-year. This regionalisation creates structural conditions for secondary markets to deepen in Mumbai, Dubai and Seoul independent of the incumbent hubs. Art SG in Singapore, expanded Frieze presence in Seoul, and the growing Art X Lagos ecosystem each represent this geographic redistribution becoming institutionalised.

How quickly that premium arrives depends on which of three paths the structural shift follows.

Base scenario: Emerging market art economies continue building infrastructure and collector depth at an accelerating pace. First-mover private collectors who establish gallery relationships and regional advisory networks in the next 12–24 months acquire at pre-premium prices, with institutional validation arriving over a 5–10 year horizon.

Upside scenario: A major Western auction house dedicates a flagship evening sale to South Asian or MENA contemporary art in New York or London, providing the liquidity event that recalibrates global valuations. The India and Gulf markets re-rate sharply.

Downside scenario: Geopolitical instability in the Gulf delays or disrupts state-backed cultural infrastructure investment. The window for pre-institutional acquisition extends but does not close; it simply takes longer to convert.

Conclusion

The structural case for building the next great collection in emerging markets is not a contrarian bet. It is the observation that geographic concentration in the art market is a lagging indicator of where cultural production and wealth formation are actually occurring. The Western canon was built by collectors who acquired ahead of institutional consensus, not because of it.

The geopolitical overlay reinforces the timing. As trade routes fragment, as Hong Kong's dominance in Asia recedes, and as sovereign cultural programmes in the Gulf and South Asia accelerate, the window for acquiring regional artists at pre-institutional prices is open but not permanent. The collector who builds in Mumbai, Riyadh or Nairobi today is not taking a speculative position on taste. They are taking a structural position on where the institutional validation machinery is heading next. The map, as currently drawn, reflects where value has been. It does not reflect where value is being created.

References

Art Basel & UBS – Global Art Market Report 2026 – March 2026

Clare McAndrew / Arts Economics – Art Market Report 2026 – March 2026

Observer / Rachel Corbett – Beneath the Art Market's Recovery, a Structural Reset Is Underway – March 2026

MyArtBroker – Art Basel & UBS Art Market Report 2026: Key Trends – April 2026

Gulf News – Indian art record: Ravi Varma painting fetches $17.9m – April 2026

Artsy Editorial – 5 Emerging Art Capitals to Watch in 2025 – January 2025

LinkedIn / Huw Lougher – The Middle East Is Building the Art Market Backwards – February 2026

Disclaimer: This article is for information and discussion only and does not constitute investment advice or a recommendation.